March 2026 Market Update

March 2026 Market Update

(edited video transcript)

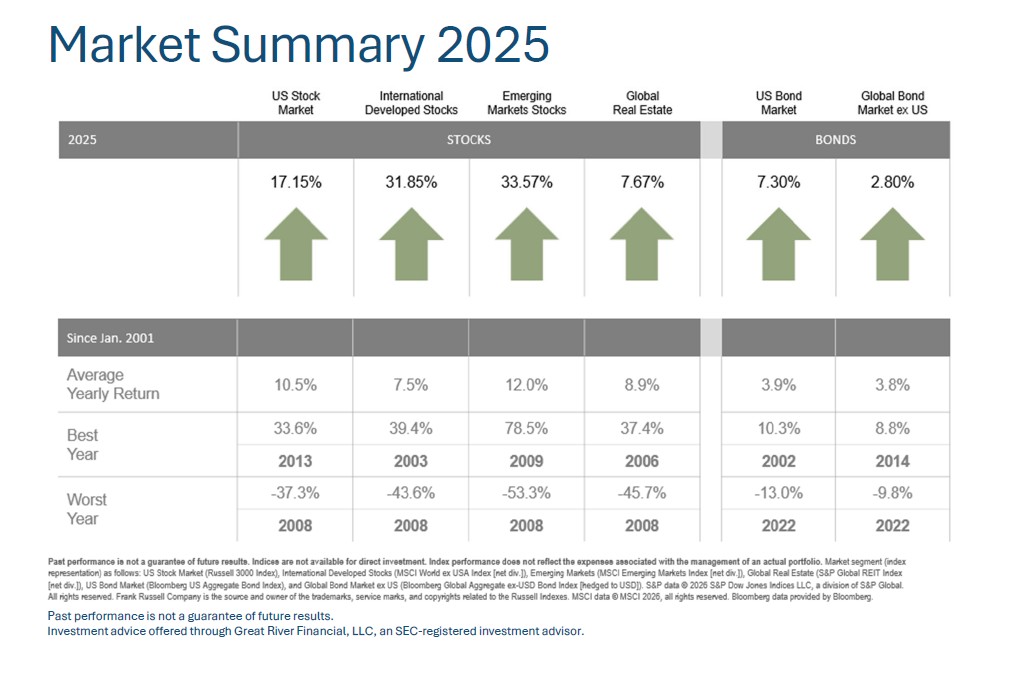

This is Josh Wolberg with Great River Financial with a market update for March 2026. Markets were strong around the world in 2025. U.S. stocks gained more than 17%, while international stocks rose nearly twice as much, up more than 30%. Global real estate and U.S. bonds returned over 7%, while international bonds kept pace with inflation at 2.8%. The dramatic outperformance of international stocks was a surprise to many. Whether they were for or against increased tariffs, few predicted the changes in trade policy would lead to international stocks increasing by nearly a third. It’s a reminder that broad diversification and disciplined rebalancing remain some of the most reliable investment strategies in all market environments. Markets often react in ways that are very different from what investors expect, especially when major policy changes occur.

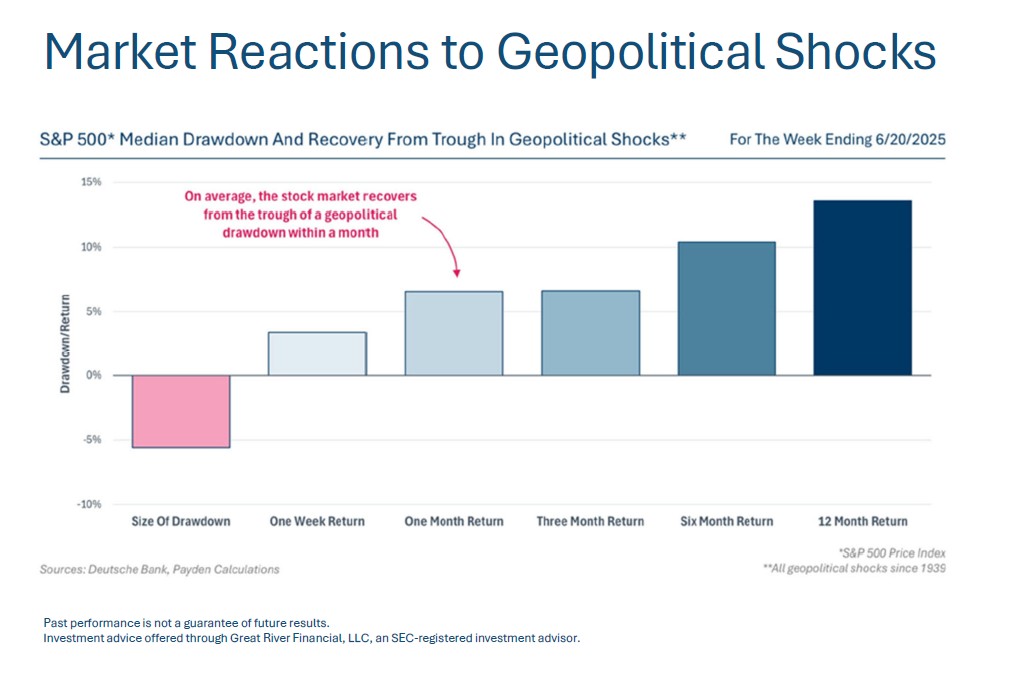

Markets tend to go down immediately after geopolitical shocks and the recent escalation with Iran is the latest example. Through the first half of March, U.S. stocks have decreased by about 2%, while international stocks have decreased by over 7%. Whether the trigger is elections, wars, terrorist attacks or major policy changes, markets historically, tend to recover very quickly from geopolitical shocks, often within about a month on average.

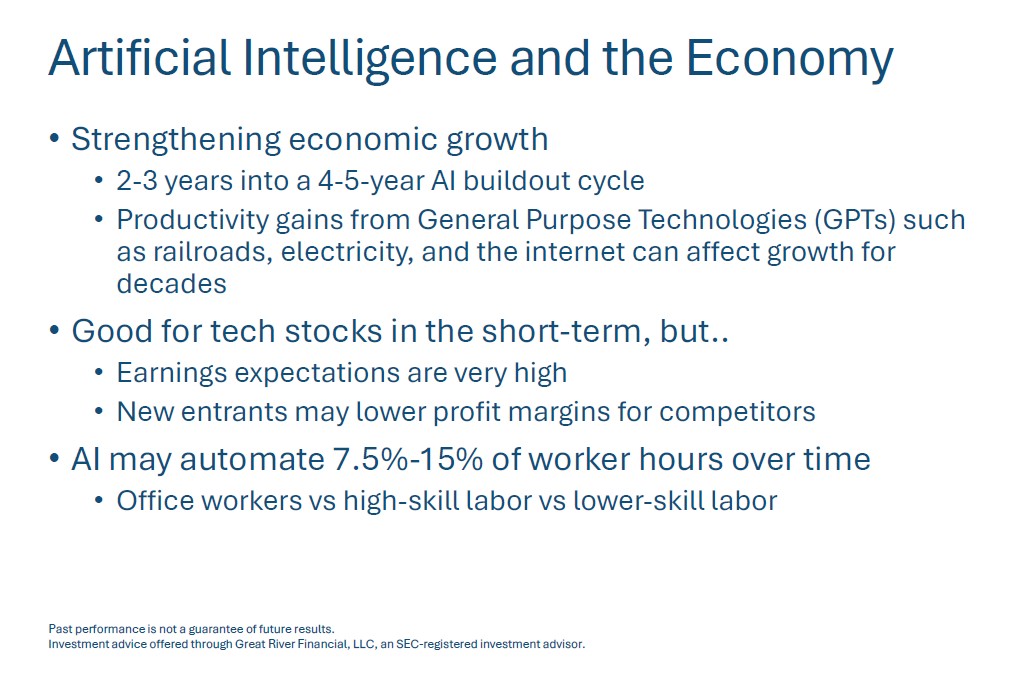

With markets setting new all-time highs, it’s natural to wonder how long the above average stock market returns can continue. Current economic growth is being driven by a rapid build out of artificial intelligence (AI) data centers combined with the optimism around the potential broad-based productivity gains from AI adoption. Technology buildouts typically take many years, and we may be only halfway through the initial wave of AI investment. This benefits industries ranging from raw materials and chip manufacturers to construction companies and energy providers. Economists sometimes refer to technologies like electricity and the internet as general purpose technologies or GPTs because they can reshape productivity across the entire economy and influence growth for decades. This economic tailwind is likely good for tech stocks in the near term, however, expectations for earnings growth may be overly optimistic. When many new companies rush into the same industry competition increases and profitability often declines. History doesn’t always repeat itself, but it does tend to rhyme. If the AI cycle resembles the internet boom and bust of the late 90s and early 2000s, a few large winners may eventually emerge while many of the other startups are acquired by larger companies or simply disappear. After the initial build out of the internet, the companies with the best performance changed from the internet companies themselves to thousands of other companies that use the internet to improve their businesses. Vanguard’s research shows this pattern is common with major technologies. For example, businesses that use electricity have historically earned far more from it than the utility companies that produce it. Lastly, AI may not eliminate as many jobs as some fear. Instead, workers who learn to use AI effectively will likely have an advantage over those who don’t. Some professions will be more susceptible than others to replacement. For the foreseeable future, AI will likely be a lot better at writing emails and computer code than upgrading electrical and mechanical systems of existing buildings.

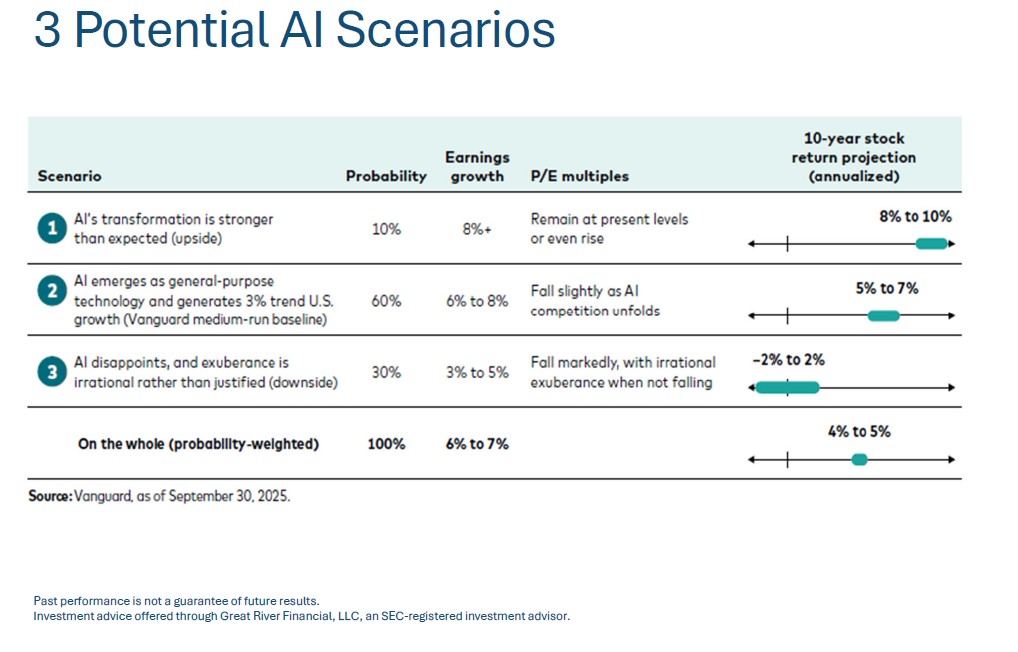

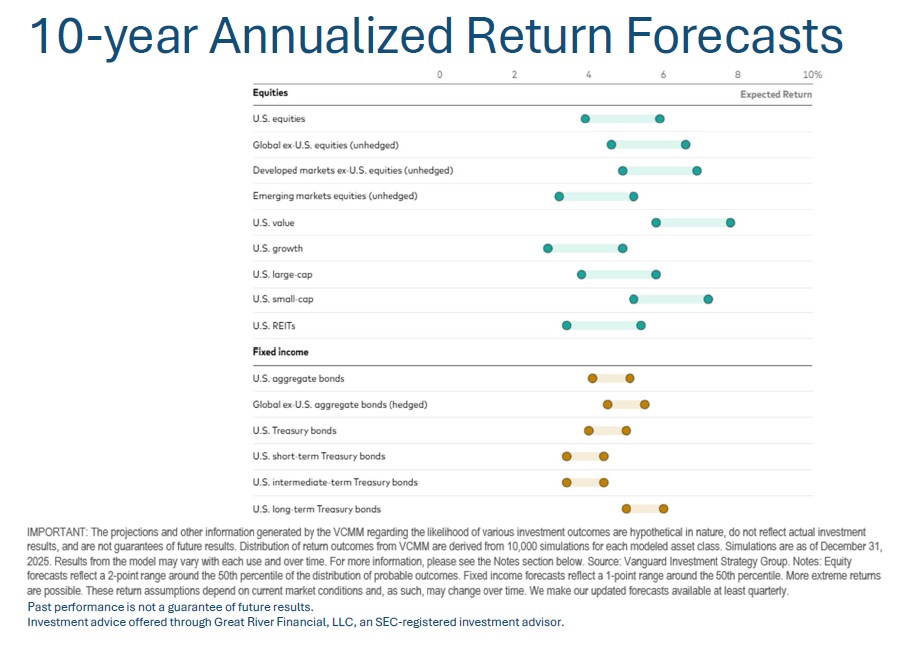

Vanguard outlines three possible scenarios for AI’s impact on the economy. Their most likely scenario at 60 % is that AI will increase productivity across the economy and help produce economic growth of around 3 % annually. Because stocks are already pricing in future profit expectations, it may lead to average returns on stocks between 5 and 7 % over the next 10 years. They think there’s a 30 % chance that productivity gains from AI disappoint, which could lead to a flat decade for US stocks. Their least likely scenario at 10% probability is that AI’s transformation is stronger than we expect, which could lead to average returns over the next 10 years being near their long-term average of around 10%.

Given the probabilities of these three scenarios, Vanguard’s annual return projections for both U.S. stocks and U.S bonds are between 4 and 6 percent for the next 10 years, but with stock prices being three times as volatile as bond prices, historically. I also agree with their view that international stocks, U.S. value stocks, and U.S. small company stocks are likely to outperform large technology stocks, given how expensive tech stocks are relative to other types of companies. 10-year treasury bond yields are around 4% and that interest rate has been one of the best predictors of bond returns over the following decade.

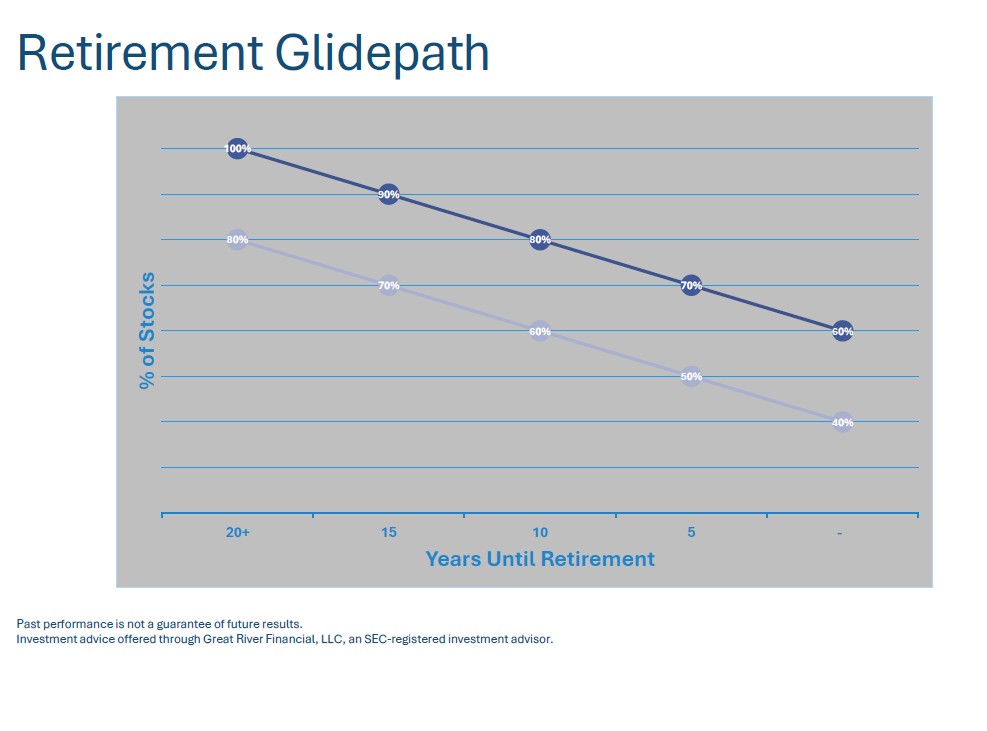

If stocks could have similar returns to bonds in the next 10 years some clients are asking if we should shift some of their stock allocation into bonds. Market conditions are an important factor when managing a portfolio, but when you need the money is even more important. Academic research finds that having somewhere between 40% and 60 % in stocks at retirement gives you the best chance of your retirement assets lasting for your lifetime while also keeping up with inflation, regardless of market environment when you retire. We implement this for clients by keeping the money you need in the next six months or so in cash. Money needed in year one through about 10 to 15 years should be in bonds and beyond 10 to 15 years should be in stocks. For those within five years of retirement, where to be in that range of 40 to 60% in stocks depends on two main factors, the current investment environment and your specific risk tolerance. When interest rates on bonds were less than 2% it made sense to be closer to 60% in stocks and 40% in bonds, even if you had a lower appetite for risk. With bonds now paying around 4% and stock valuations relatively high, it may make sense to move towards the lower end of that stock allocation range, depending on how you respond to market volatility.

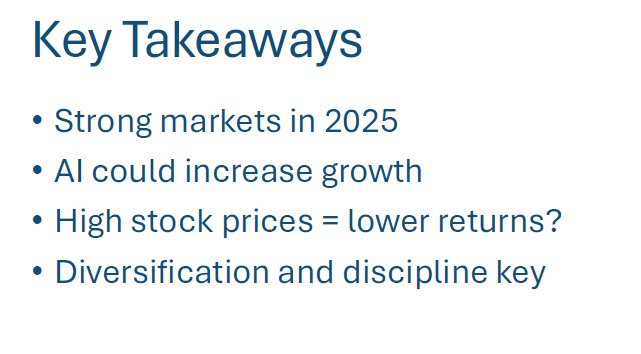

So, the key takeaways. Markets were strong globally in 2025. AI investment could support economic growth for many years. High stock valuations suggest more modest returns going forward. All of this makes diversification and disciplined balancing more important than ever. We’ll continue to monitor market developments, rebalance portfolios and share updates along the way. Feel free to call or schedule a time with us, if you would like to discuss anything further. If you found this helpful feel free to share it with a friend or family member who may benefit. As always, stay curious, my friends.